Construction loans

Finance Your Home Build from Start to Finish

Planning to build instead of buy? Construction loans provide flexible financing to cover land, materials, and labor. Then transition into a long-term mortgage once your home is complete. Whether you’re working with a builder or managing your own project, we’ll guide you through every step.

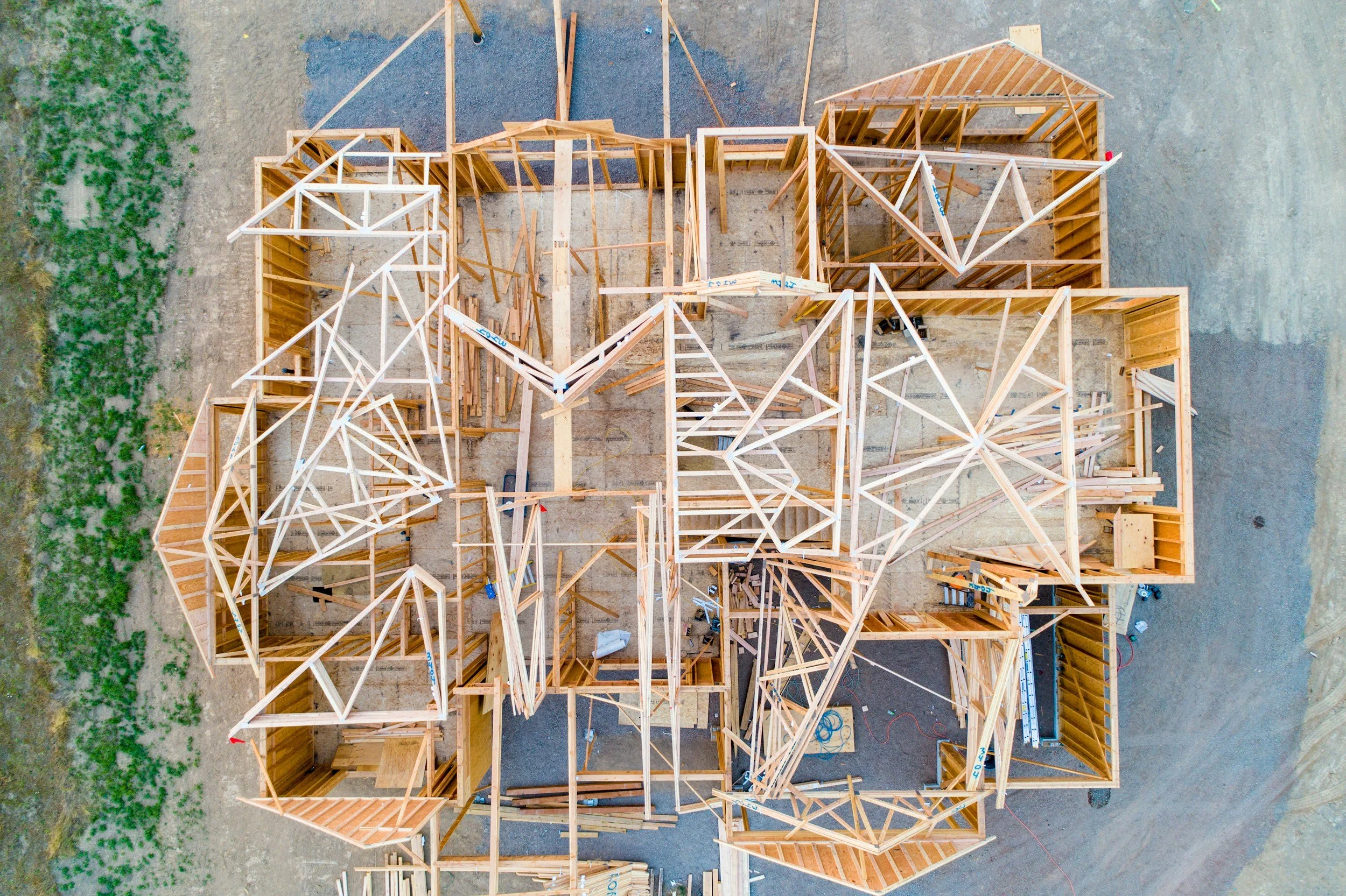

A construction loan is short-term financing used to fund the building of a new home. Funds are typically released in stages called draws,as construction progresses. Many borrowers choose a construction-to-permanent loan, which converts into a standard mortgage after the build, simplifying the process with a single closing.

What Is a construction Loan?

a construction loan can be used for:

Building a Primary Residence

Working with a Licensed Builder

Purchasing Land and Building

Construction-to-Permanent Financing

Benefits of a construction loan

FINANCE THE FULL BUILD

ONE TIME CLOSE OPTIONS

FLEXIBLE TIMELINES AND DRAW SCHEDULES

HOW TO QUALIFY for a CONSTRUCTION Loan

If you’re asking “what do I need to qualify for a construction loan?”

Here’s a general guide:

Credit score: Typically 620+ (varies by program)

Down payment: 3%-20%, depending on ownership, program, and equity

Detailed plans & budget: Builder contract, blueprints, timeline

Licensed builder approval (in most cases,depending on state requirements)

Stable income & reserves

We’ll review your plans and finances together to determine the best path.

FAQs

How does a construction-to-permanent loan work?

1

It starts as a construction loan and automatically converts into a traditional mortgage after the home is complete, often with one closing.

Do I make payments during construction?

2

In many cases, payments are interest-only based on the amount drawn during the build phase.

How long does the construction phase last?

3

Typically 6–12 months, depending on the project.

Can I buy land and build with one loan?

4

Yes, many construction loans allow you to finance both land purchase and construction.